Would you like a free review of your loans to ensure they are still competitive?

Please call Peter, David or Simon on 03 9882 2500 or email;

Please call Peter, David or Simon on 03 9882 2500 or email;

Click to view our range of mortgage calculators

We have written to our clients in recent months to keep them informed about significant changes in the Australian investment loan and interest-only loan market.

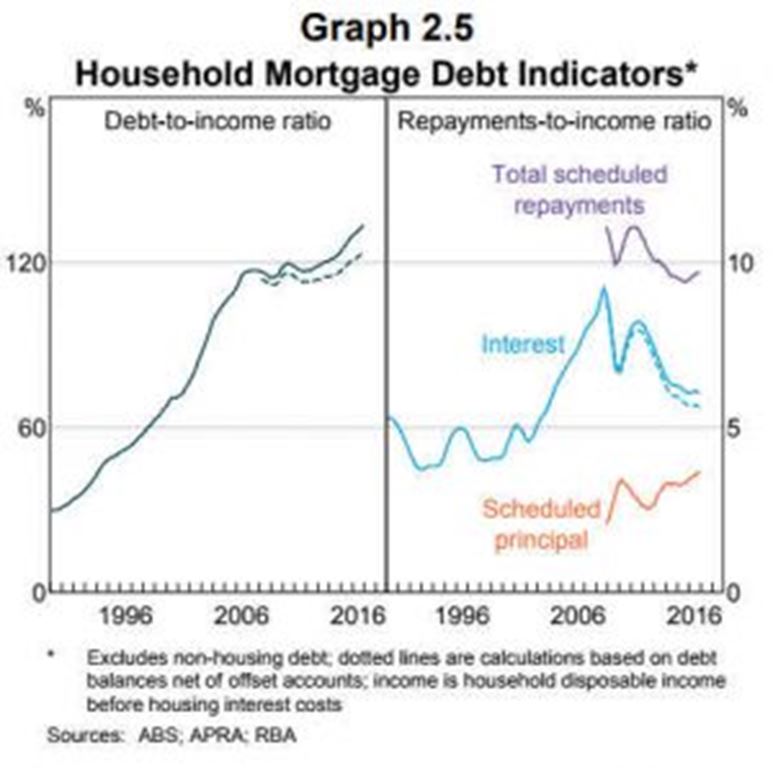

The Australian Prudential Regulation Authority (APRA) – the prudential regulator of the Australian financial services industry – has been concerned about the strong growth of lending to property investors and interest-only borrowers for some time; particularly in Melbourne and Sydney. APRA is concerned that a downturn in property prices could lead to an increase in loan defaults so they want to see a higher proportion of principal and interest debt reduction in Lender portfolios.

The increase in investment lending has also influenced a large rise in interest-only loans; primarily for investment purposes but interest-only lending has also increased for owner occupied loans.

As a result, interest rates on investment and some owner occupied loans, in particular interest only and Line of Credit facilities, have increased across all lenders.

For simple home loans, the difference between Interest Only repayment rates and Principal and Interest repayment rates is already around 0.50% pa variable (the rate is higher for Interest Only).

There has also been a host of changes to lending policies; all driven by APRA and aimed at ensuring a sustainable growth in the home loan investment sector and improving the strength of Australia’s financial services industry.

APRA’s New Capital Requirements

In July APRA announced their new requirements for the majority of Lenders in Australia to increase the amount of capital they currently have, so that they meet the “unquestionably strong” benchmark recommended in the 2014 Financial System Inquiry (FSI). The four major banks will be required to raise large amounts of capital and whilst they have two and a half years to achieve their imposed targets they (together with other Lenders) may need to raise their interest rates to cover the increased costs influenced by this requirement.

Interest Only Expiry & Extensions

In conjunction with the above, extension of Interest Only periods following their initial expiry is becoming more difficult with many lenders now treating this as a “credit critical” change, and requesting full financial information to reassess the applicant’s servicing capacity, noting that any interest only period reduces the available term thereafter, over which the loan must be repaid. The loan must be contracted in such a way so that it is fully repaid within the contracted term. A 30 year loan with an interest only period of 5 years results in the loan having to be repaid over the remaining 25 years. For loan assessment/approval purposes the Interest Only period essentially reduces your borrowing capacity.

Line of Credit Facilities

The rate increases are also applicable to Line of Credit facilities which are “interest only” by nature, and now carry a premium well above the Standard Variable Rate for standard loan products.

If you have an Interest Only Loan or a Line of Credit and you are concerned by the recent interest rate increases please contact our office to discuss a possible switch to a Principal and Interest loan. The switch may be as simple as a one page switching request and free of any bank fees.

If we can assist please call Peter, Simon or David on 03 9882 2500 or email;

Purchasing your perfect home or investment property is an exciting and challenging journey, and usually is one of the largest investments in your life! It is therefore important to remain level headed throughout the excitement, to understand what you may be able to afford, and to engage with a professional to help you through the various stages of buying.

Talking to your Finance Broker about obtaining a Pre-Approval is the best (and safest) way to start this journey.

A Pre-Approval, otherwise known as an Approval in Principal (AIP) can be obtained by speaking to First Point Group about your property goals. We can then work with you to shape your potential borrowing capacity, and the broader strategy. We then research the market, discuss and agree the most suitable lender for your needs, and then we handle all of the paperwork and bank/lender discussions for you.

Examples of documents required for Pre Approval are:

• Proof of income (pay slips, tax returns if you are self employed)

• Monthly living expenses (we offer a template to assist you in allowing for all of your normal living costs)

• Information about any existing debts/commitments such as loans, credit cards, HELP debt

Benefits:

There are many benefits of organising a Pre-Approval prior to buying or even locating the right property. For example:

• It provides an indicative guide on how much you can afford to borrow, and therefore how much you may be able to spend on a property

• Financial Safeguard – avoids a costly situation, where you may have won a property at an auction, later to discover you cannot satisfy a lender’s ongoing servicing requirements or loan conditions

• It allows you to “shop with confidence” and bid at an auction should your dream home come onto the market

• Handy tool for price negotiations – It shows your estate agent that you are serious about buying a home. Some agents won’t spend their time showing you homes in case you don’t come through with the financing

• The approval valid for up to 3-6 months. Your circumstances, and the home loan market, can change rapidly. First Point Group ensures that you have a clear idea of how long your home loan Pre-Approval is valid for. The time frame will depend on the relevant lender and it is usually a simple process to update the Pre-Approval

Proceeding to Formal Approval:

The Pre-Approval is simply an indication of your ability to borrow funds from a lender, based on the information provided at that time. Once you have successfully found your dream property, First Point Group’s experienced team can assist to progress your loan to a Formal Approval, and prepare for settlement of the property.

To find out more about our 10 Step Loan Process please click here.

Taking the time to speak to experienced professionals such as First Point Group, and preparing yourself through every aspect of your property search, can assist to make the process of finding your dream home a positive and pleasant experience.

We are finally starting to see the first signs of the Melbourne property market slowing. Recent figures from CoreLogic, released at the start of June, showed property prices in Sydney and Melbourne fell by 1.3 per cent and 1.7 per cent, respectively, during May 2017.

Although this is a positive sign for those struggling to enter the property market, particularly first home buyers, the ratio of property values to income growth still leaves many people facing great difficulty to purchase a home in Melbourne and Sydney.

One option for people who want to live in a capital city and purchase a property, but cannot afford to do so, is to rent where you live and purchase an investment property within a more affordable area. This allows you to rent wherever is the most suitable for you in terms of work or study, and still benefit from the investment returns that property can provide over time.

This approach has become increasingly common in recent years. Surveys have shown that this approach has become so popular, LJ Hooker have actually trademarked the term “Rentvesting” – The act of renting where you want to live, and buying where you can afford.

This approach allows for terrific flexibility and can be a great way to enter the property market, however first home buyers should keep in mind that if they take this approach, they will not be entitled to the first home buyers stamp duty concessions or grants that are normally offered for purchasing or building an owner occupier home to live in. These benefits may still be available for a future owner occupier purchase, however we recommend that you seek the advice of your local State Revenue Office.

On the positive side, you may be entitled to some negative gearing benefits, tax deductible interest and a rental income boost that will assist with saving for another property. We always recommend you seek advice from an Accountant before embarking on any major investment, and we can recommend an Accountant for you if required.

The complete Reserve Bank of Australia ‘Financial Stability Review April 2017’ can be viewed here

Please contact us to discuss which method of finance is best suited to your needs

You are considering selling your current home, and buying another. Ideally you would like to move straight out of your current home into the new one, which would mean both settlements occurring on the same day. But how do you finance the purchase of a new home if you cannot align the settlement dates?

There are a couple of scenarios to consider:

1. The Sale settles first – In this case, financing is easier because you can use the sale proceeds to put towards the purchase, however, where will you live in between the two settlements?

a. You could temporarily move into another house (eg. a rental, or with family). This is often the only solution however you need to consider the obvious double handling with removalists etc

b. You could potentially negotiate with the Purchaser of your home, to let you rent the property off them for the period in between settlements

2. The Purchase settles first – You already have a home loan, and you don’t have access to the equity / cash from your home because it has not yet settled! In this case you need to consider a Bridging Finance solution

How Does Bridging Finance Work?

Bridging Finance enables you to borrow up to 100% of the purchase price to settle on a new purchase, whilst you work on selling your current home, however, there are a few important elements of bridging finance to be aware of.

Bridging finance is not for everyone

As a ‘rule of thumb’ it is most often only a viable solution if you have built up equity of at least 40% of your existing home’s value, before you attempt a bridging loan. Otherwise, the total amount of lending that you need to settle on the new property (plus your existing home loan) may be more than the maximum loan amount available.

How do you borrow 100%?

Whilst you can also contribute some cash towards the new purchase, the bridging loan is often used to cover 100% of the purchase price and relevant stamp duties. The loan is secured against both the new home and the existing home. Even though bridging may only be required for a short term, the “total loans” (new and existing) cannot exceed 80% of the “total property value” (for both existing and new properties).

Potential Issues

To complicate the numbers further, various lenders use different models to calculate the value of a bridging loan. One common model includes a 15% allowance against the potential sale price of your existing home – In other words, say you think you could sell your home for $800,000, some lenders will assume (for the sake of approving or declining the bridging loan) that you will only sell for $680,000. This immediately impacts whether bridging finance is viable, and reinforces the 40% equity guide discussed earlier.

How do repayments work?

The loan is often split into two parts:

1. The loan amount that you would eventually need once your sale has gone through (ie. the ongoing home loan). Repayment on this loan are usually Principal and Interest over the standard term of 30 years (ie. normal home loan repayments)

2. The ‘bridging loan’ which covers the rest of the purchase price. This loan allows for interest to ‘capitalise’ on top of itself – in other words repayments on this loan are optional. However, the more interest that accrues, the less money you will receive from the sale proceeds

What are the risks?

The obvious risk is that for whatever reason, you are unable to sell your old home. Bridging loans typically have a maximum term of 6 months; after this date the lender may enforce a monthly repayment on the bridging loan (which can become a significant cash flow burden), and if the sale process still does not gain some traction, the lender may reserve the right to take charge of the sale process, which can result in a lower sale price.

If structured correctly, with realistic time frames and price estimates, bridging finance can ease the pressure of matching up settlement dates, and give you time to sell your existing property whilst securing your new one.

When First Point Group consider a bridging scenario, we outline all of the abovementioned figures for you to ensure you understand the benefits and the costs involved in bridging.

Please call Peter, David or Simon on 03 9882 2500 or email;

First Point Group recently structured a development finance application to assist with the development of 6 townhouses on a main highway in the Western Suburbs. The clients were not ‘developers’ as they had regular ‘day jobs’, so this case presented with several hurdles:

a) Prior experience of the client – Our clients had a relatively brief ‘CV’ having only really completed one other smaller development, yet they owned a number of other residential properties which assisted in demonstrating their ability to generate wealth through successful property investment

b) Prior experience of the builder – In this case the client outsourced the construction to an arm’s length, ‘fixed price builders contract’. Fortunately, the builder had a long history of delivering projects on time and on budget

c) Reliance on rental income – In this case the proposed loan would not meet the lender’s serviceability guidelines without utilising the rental incomes from the proposed townhouses, however these were complimented by other rental incomes and wages

d) Pre-Sales – Ordinary lender/bank policy would be to pre-sell (off the plan) around 100-110% of the loan amount to arm’s length buyers. In this case, the client much preferred to retain as many of the 6 townhouses as possible, and we agreed with the lender that a pre-sale of only two townhouses would be acceptable (2 townhouses equivalent to only 60% of debt cover).

To achieve this several other factors were negotiated:

a. The ratio of Loan to Total Development Cost (Loan to TDC) had to be low (under 60%)

b. Return on costs had to be as high as possible – In this case the ‘profit margin’ was reduced due to recent buoyancy in the property market however the loan would also be very well secured as per below;

c. The Loan to Value Ratio (LVR %) at the start of the project had to be low – In this case, FPG was able to refinance other existing loans in order to unencumber the development site, dramatically reducing the starting LVR.

First Point Group recently financed the import of plant & equipment (Co-Extruders) from China using a Commercial Building as security to support establishment of an Import Letter of Credit.

Upon arrival of the goods we then were able to clear the Trade Finance using a Chattel Mortgage/Hire Back facility using the equipment as the only security. The Commercial Building was then released as security as the trade finance was cleared.

This was a complex transaction where we added significant value to allow the increase in capacity at the client’s plant, and allow them to enter new markets in Australia and New Zealand.

Please call Peter, David or Simon on 03 9882 2500 or email;

Interest Rate Update – August 2017

Interest Rate Update – August 2017