Give Us A Call

If we can assist please contact Peter, David or Simon on 03 9882 2500 or email

The biggest mistake you can make when managing your credit card is choosing the wrong card in the first place. The best way to choose the right card is to ask yourself how you intend to use it.

If you belong in the first category and you clear the balance in full each month, you need to select a credit card with the longest possible number of interest-free days and the lowest annual fee and reward program. Look at whether the card will provide an annual fee waiver if you spend more than a set amount each year or if the card is part of a Home Loan Package. The interest rate is irrelevant because you’re never going to incur an interest bill!

If you are one of the many cardholder’s who fall into the second category, the interest rate is the most important factor so you need to select a card with the lowest available ongoing interest rate and with a low/waiver of annual fee. Be wary of cards offering honeymoon rates, including the many cards offering the 0% balance transfer. Check the rate the card will revert to at the end of the special offer period, how interest and ongoing payments during the honeymoon period are calculated. Also check how interest and ongoing payments during the honeymoon period are calculated. There are some excellent low interest cards available, but remember it is important to destroy and close your old card account once your new card becomes active.

When selecting a 0% or 1% balance transfer etc it is ideal to make every effort to fully clear the debt during the zero or low rate period and put the card away in a safe place so you aren’t tempted to use it for other purchases during this period.

One of the most important points to remember:

Even if you can’t clear your balance in full you should make every effort to pay more than the minimum monthly payment specified on your statement. If you only pay the minimum, depending on the size of your debt and interest rate, you may find it virtually impossible to ever have a zero balance, thus incurring higher interest costs.

A high Credit Card debt also can effect your borrowing potential if you are wishing to increase your personal or investment borrowings. Lenders normally include your credit card limits in their financial assessment, therefore think hard next time you accept that new card offer in the mail!

Also remember all Banks/financial institutions now offer debit cards which can be used the same way as a credit card but you are using your own funds.

If you have equity in your home and do have a large credit card debt it may be time to seek an increase, redraw on your existing home loan or even seek approval of a small Line of Credit to clear the debt in full.

If we can assist please call Peter, David or Simon on 03 9882 2500 or email;

Are you a property owner with a business as well? We can help you with commercial and asset finance too.

One of the basic tenets of work/life balance is: ‘Don’t bring your work home with you.’ But what if you could bring your home to work? It’s a scenario that home owners with a business should consider when seeking commercial or asset finance.

Three common types of business finance are:

Business loan: the lender loans money to the business for its operations and the business repays the lender with interest.

Commercial investment: the lender loans money to the business to invest in an asset, including real estate. The asset is often used as security and the repayments attract interest.

Chattel mortgage or equipment loan: the lender loans money to the business to purchase equipment or vehicles, which are used as security. The business makes a series of principal and interest loan repayments in return.

When it comes to purchasing an asset, lenders will often use the asset as security against the business’ debt. In some cases, however, such as with the purchase of equipment or vehicles where the assets may depreciate over time, the asset itself may not be sufficient security. In other cases, for instance when a business seeks a loan for operational needs, there may be no security.

Sometimes the more security you can offer a lender, the lower the interest rate it will charge and vice versa. Unsecured loans often attract the highest interest rates since there is more risk to the lender. If you’re a home owner with equity in your property, you may be able to use this equity as security to leverage a better rate on your business loan.

As with mortgage rates, commercial and asset finance rates will vary from business to business. Lenders will look at things such as industry volatility, how long you’ve been in business and your financial records to determine the risk factors that will contribute to their loan terms. First Point Group can offer an unbiased view on whether your property is suitable to be used as security, how much equity you can use and how this might affect different loans from different lenders.

We can assist you with so much more than just your home loan. Don’t leave business growth until the future – explore how commercial and asset finance can work for you today.

If we can assist please call Peter, David or Simon on 03 9882 2500 or email;

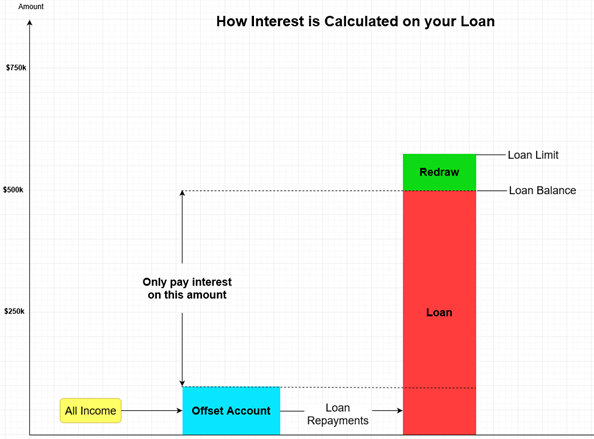

Often people ask us about Home Loan redraw vs offset and if redraw would suit them better or offset. Well, the good thing is that most of the Lenders we deal with all offer redraw and offset as part of their Professional Packages. Even the budget type loans offer redraw but do not offer offset capability.

Definitions

Redraw

A redraw is allowed on variable rate loans when you are ahead or in front of your loan program i.e. your loan balance is less than what the Lender expected or scheduled it to be at a point in time.

Redraw effectively allows you to withdraw funds back up to the amortization line for any purpose without questions from the Lender. It can be effected electronically/internet, over the phone or at a branch or sometimes Australia Post and funds be transferred to your elected bank a/c within 24 – 48 hours. Redraw is normally free.

Some people use redraw to draw funds for renovations or at times investments. You need to be careful if you redraw for investment purposes, in particular if your loan is a home loan/owner occupied. This is due to the tax office having difficulty assessing what part of your loan, if it is one loan, is tax deductible or not. If you redraw for investment purposes it may be best to request your loan to be split at the time into Investment and Home Loan so there is a clear delineation between Owner Occupied non tax deductible interest and tax deductible investment loan interest.

You could also request that a separate Line of Credit be put in place for the Investment transaction again to clearly separate it from the Home Loan. Some people used 100% offset for this key reason so the funds are in offset against the loan rather than in redraw. Refer below.

100% Offset

This is where 100% of your transaction account at your same Lender is fully offset against your home loan or investment loan. Normally only used against Owner Occupier Home Loans because of a Home Loans non tax deductible nature.

Example

$300,000 Home Loan balance

$10,000 in offset a/c

Net Loan Balance after offset $290,000.

Interest is only charged by the Lender to the net loan balance after offset. This is applied on a daily basis so it depends on your transaction a/c balance and loan balance each day. Obviously if you owe less on a net balance basis, then any repayments you make are applied to the net balance giving you a greater impact on the principal/capital amount of the loan.

Offset is used by the majority of our clients who have home loans that are non tax deductible. We also find people that carry large balances in an offset need to be disciplined in use of their funds. Some people prefer to place their surplus funds in redraw for this reason as the feel it is that little bit harder to get to.

Whichever way we encourage you to go, both redraw and offset end up providing excellent financial outcomes and also great flexibility.

Like other superannuation funds, SMSF’s are primarily used to build wealth for retirement. SMSF’s are different from other superannuation funds as all members are also trustees (or trustee directors, if the SMSF has a corporate trustee). Members are responsible for running the fund including the documented strategy for investing the fund’s assets, paying benefits and meeting the administrative and compliance requirements of the fund.

Changes to the Superannuation Industry (Supervision) Act 1993 (Cwlth) and Regulations (SIS Act) during late 2007 allow SMSF’s to borrow money from a Lender to purchase investment assets such as residential & commercial property. This ability to borrow can build on the taxation advantages currently available to superannuation funds (refer to your Accountant) and can help a fund to acquire a larger and more diversified portfolio of investments with a view to successful long term wealth accumulation.

Since early 2008, First Point Group has completed many successful SMSF Loan/Borrowing transactions with Lenders to assist clients in this rapidly growing area including:

• Purchase of an owner occupied commercial building

• Purchase of a waterfront investment home

• Purchase of three residential townhouses

• Purchase of a factory from a related family trust

It is important to note that the ATO have advised (9/2011) previously that SMSF’s will be able to improve properties held within funds, providing that borrowings are not used to renovate. You will need to speak to your Accountant to understand the full ATO implications of this change.

If we can assist please call Peter, David or Simon on 03 9882 2500 or email;

Approximately this time last year I was enjoying three weeks of trekking through Patagonia – a vast and diverse region with dramatic mountain formations, smoky volcanoes, flat barren lowlands and expansive ice fields. Shared by both Chile and Argentina this beautiful part of the world is not often spoken about as a destination for adventure and tourism, unless you had plans to visit Antarctica and therefore fly or sail into Punta Arenas before heading south. This was my original intention – to spend time in Antarctica, but the high cost together with the opportunity to explore Patagonia meant you will read about my trip to the ice a number of years from now. Whilst on the subject of ice, the Patagonia ice field is the world’s third largest reserve of fresh water.

14 other trekkers, well organised by a good friend, Wayne Enright from Free Spirit Adventures (www.freespiritadventures.com.au), commenced with a flight into Punta Arenas followed by a three hour bus ride to Torres del Paine National Park where our adventure began. Based at a very comfortable eco camp at the southern tip of the Andes we hiked through many impressive mountains – home to some of the world’s most classic trekking routes. The sun often set around 11.00pm, providing plenty of time at the end of the day to enjoy the spectacular views whilst drinking some excellent Chilean reds.

A week later we were driven further north to a small and beautiful trekking village called El Chalten – an excellent base providing shelter and fine Argentinian reds to enable us to spend 4 days exploring the Los Glaciares National Park and the incredible Mt Fitzroy (3,405 metres).

A highlight of our trip was a hike on the famous Perito Moreno Glacier – one of the largest glaciers in South America. It is also of scientific significance as it is one of a few remaining advancing glaciers in the area, said to be “growing” at a rate of 2 – 3 metres per day. Most of the world’s glaciers are located over 2,500 metres above sea level. In Patagonia many glaciers originated at 1,500 metres above sea level, flowing down to 200 metres – meaning they are more easily accessible and an important reason why Patagonia will increasingly become a desired tourist destination.

Whilst I am not overly excited about cold places I do enjoy the opportunity to step outside my comfort zone every so often. Patagonia provided a terrific experience and (thankfully) a window of some relatively warm weather for the majority of our time in this beautiful part of the world.

If we can assist please call Peter, David or Simon on 03 9882 2500 or email;

Interest Rate Update – February 2017

Interest Rate Update – February 2017